Deposits dropping once more for lower credit classes for BYOD and SIM-onlt

Just under a month ago, we reported that T-Mobile had changed its deposit pricing based on credit classes. Deposits were dropped to just $50 for credit classes N, H and D, whereas class I was dropped to $50 for the first 3 lines, with a $100 required for lines 4 and 5. These changes went live on February 7th.

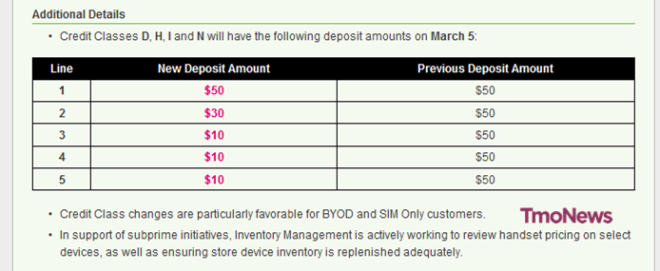

From March 5th, it looks like they’re changing again. We’ve received some information claiming that deposits are changing again. The information we have is below:

It looks like – from March 5th (2 days time) – only the first line for those classes will come with a required $50 deposit. The second line will cost $30, with each of the following lines (3-5) only requiring the customer to cough up $10. Dropping down incrementally, instead of rising.

Obviously, if you have excellent credit, this won’t affect you at all. But for those with less than excellent credit, it’ll mean not having to cough up so much cash up front. Considering so many devices are available with $0 down, paying just $50 doesn’t seem like that big a deal.

What this move says to me is that T-Mobile is moving aggressively to sign up as many people to its network as humanly possible. If – for instance – a customer can’t get a device with a rival carrier because of his/her credit, being able to come over to Magenta and pay just $50 to get a device is such a relief. Undoubtedly, the work of T-Mobile’s retail staff will become easier too.

[Update: Seems like these changes might only be for those who bring their own device or pay full retail price for their phones and get SIM-only. Any retail staff out there, get in touch after the 5th and let us know the full picture if you can. Email: cam@tmonews.com]

What do you make of these changes?