Credit Score changes allow up to 5 lines and reduced deposits for lower-scoring customers

One of the biggest challenges for phone retail staff when selling contracts is signing up lower credit class customers. In T-Mobile’s case specifically, deposits are required for anyone with low credit score. This is pretty common practice, and not only in the States. As a former T-Mobile UK staff member, it was one of the worst feelings having worked through finding the right phone, the right plan, making them happy only to turn around and tell them they’ve been declined or require a deposit to allow them to take the plan.

One of the biggest challenges for phone retail staff when selling contracts is signing up lower credit class customers. In T-Mobile’s case specifically, deposits are required for anyone with low credit score. This is pretty common practice, and not only in the States. As a former T-Mobile UK staff member, it was one of the worst feelings having worked through finding the right phone, the right plan, making them happy only to turn around and tell them they’ve been declined or require a deposit to allow them to take the plan.

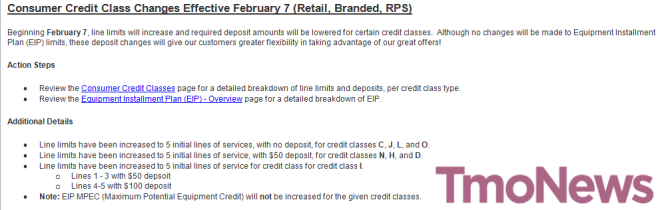

T-Mobile US – from February 7th (yesterday) – changed the way it works out deposits and the number of lines available to those customers. As you can see from the internal email above, the changes include credit classes C, J, L, O, N, H, D and I. Details on the changes are as follows:

- Line limits for classes C, J, L and O have been increased to 5 lines of service with no deposit required.

- Line limits for classes N, H and D have been increased to 5 lines of service with $50 deposit required.

- For class I, 5 lines are available. The first 3 lines will be subject to $50 deposit while lines 4 and 5 require a $100 deposit.

We’re reminded, finally, that although the line limit and deposit are being changed, the maximum potential credit allowed on EIP will not be changing for any of the credit classes.

The intention here is to make it easier for everyone to get a phone on EIP without being too much out of pocket from paying a deposit. This in turn makes the sales people’s work less frustrating, and the consumer experience more enjoyable. As mentioned previously, these changes started yesterday on February 7th. Tmo staff, let us know how these changes affected you.